")

IMPORTANCE OF THE TAX ADDRESS IN FOREIGN TRADE OPERATIONS

Recently, the list of companies to which the IMMEX was suspended was published in the Official Gazette of the Federation, among which 100 companies that failed to comply with the requirement established in article 11, section III, subsection c) of the IMMEX Decree stand out. that is, that their fiscal domicile and the domiciles in which they carry out their operations under the Program, are registered and active in the Federal Taxpayers Registry and, as a consequence of this, due to the lack of presentation of the annual report foreseen in article 25 of the same order.

ARTICLE 11.- The Secretariat, with the prior favorable opinion of the SAT, will authorize a Program to the moral person that complies with the provisions of this Decree, in accordance with the following:

…

III. The applicant must have the following:

…

c) That their fiscal domicile and the domiciles in which they carry out their operations under the Program, are registered and active in the Federal Taxpayers Registry.

The foregoing derived from the mandate that article 29 of the IMMEX Decree itself indicates to the Ministry of Economy, which is to verify annually that the fiscal domicile requirement continues to be met.

But this situation leads us to the following question, what is the importance of the fiscal domicile in foreign trade operations?

WHAT IS THE TAX ADDRESS?

In the first place, we must understand that FISCAL DOMICILE is the place that the legislator indicates to the taxpayer for all cases derived from the substantive tax relationship. Its foundation is found in article 10 of the CFF.

Second, the FISCAL ADDRESS constitutes an attribute of the RFC, so it must be a reliable piece of information so that the authority has a certain location of the taxpayers, in which it can know its operation.

The FISCAL ADDRESS serves the Authority to:

- Locate the taxpayer

- Access Accounting and foreign trade operations

- Notification of Administrative Acts.

- Carry out collection actions through the administrative enforcement procedure.

- Determination of non-existent or simulated operations.

- Review of tax receipts and cancellation of CSD.

- Actions in matters of Foreign Trade.

- Violations in relation to the RFC.

- Tax offenses related to the RFC.

- Verification Faculties.

- Apply enforcement measures.

TAX ADDESS AND FOREIGN TRADE

But the TAX ADDRESS DOMICILE is not limited to operations related to the RFC, since it becomes relevant when the current regulations related to foreign trade are analyzed:

For example, if you wish to import or export, you must register in the Register of Importers, being one of the requirements according to the Procedure File 5/LA, that the FISCAL ADDRESS must be in the status of "located in the RFC" or in "verification process".

5/LA Procedure instructions to register in the Register of Importers

Conditions:

- Be registered and active in the RFC.

- Have a valid e.signature.

- Be up to date in meeting your tax obligations.

- The fiscal domicile must be found as located in the RFC or in the process of verification by the ACIA.

- The status of the Tax Mailbox must be "Validated".

- Have a customs agent, customs agent and/or legal representative, who will carry out their foreign trade operations, in compliance with the obligation set forth in article 59, section III, second paragraph of the Law.

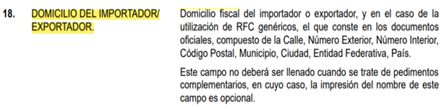

The TAX ADDRESS will be reflected in your import or export petitions, as indicated in Field 18 of the Instructions for filling out the Petition, of ANNEX 22 OF THE GENERAL RULES OF FOREIGN TRADE FOR 2022.

SUSPENSIONS AND CANCELLATIONS

Now, although it is true that the TAX ADDRESS is an attribute of the RFC, not having it updated or that the authority determines a status of NOT LOCATED or NON-EXISTENT has consequences in your operation, depending on the standards, programs and/or registries in which your company operates.

For example, with regard to the General Rules on Foreign Trade, they are grounds for suspension of the Register of Importers of Specific Sectors or in the Register of Sectorial Exporters, when they make a change of fiscal domicile or make the change after the start of powers of verification or when they are not located at their fiscal domicile or this does not meet the characteristics of article 10 of the CFF or when the fiscal domicile of the importer, indicated in the petition.

Causes of suspension in the registers

1.3.3. For the purposes of articles 59, section IV and 144, section XXXVI of the Law and 84 and 87 last paragraph of the Regulation, the suspension in the Register of Importers and, where appropriate, in the Register of Importers of Specific Sectors or in the Register of Sectorial Exporters, to those who introduce or extract goods from the national territory that are in any of the following cases:

…

VII. Make a change of tax address or make the change after the beginning of verification powers, without presenting the corresponding notices to the ADSC, in accordance with the terms established in article 27, Section D, section II of the CFF.

They are not located in their fiscal domicile or it does not meet the characteristics of article 10 of the CFF, or the taxpayer's fiscal domicile or any of the places indicated in article 29, section VIII of the CFF Regulation, are in the event of non-existent .

The name, denomination or business name or domicile of the supplier abroad or fiscal domicile of the importer, indicated in the request, in the CFDI or equivalent document presented and transmitted, in accordance with articles 36-A, 37-A and 59-A of the Law, are false or non-existent or when at the address indicated in said documents, the supplier cannot be located abroad; recipient or buyer, abroad.

In the IMMEX Decree, that the company is not located at its fiscal domicile or at the domiciles registered in the Program to carry out the operations under it, or said domiciles are in the event of not being located or nonexistent; or the SAT determines that the name or fiscal address of the supplier or producer indicated in the petitions, invoices or the information transmitted in terms of the Law, are false, non-existent or not located, is a cause for cancellation.

ARTICLE 27.- It is cause for cancellation of the Program that the company is located in any of the following assumptions:

…

III. It is not located at its fiscal domicile or at the domiciles registered in the Program to carry out the operations under it, or said domiciles are in the event of not being located or non-existent;

…

1. Submit false documentation, altered or with false data, or when the SAT determines that the name or fiscal address of the supplier or producer, recipient or buyer abroad, indicated in the petitions, invoices or the information transmitted in terms of the Law, are false, non-existent or not located;

ARTICLE 27.- It is cause for cancellation of the Program that the company is located in any of the following assumptions:

…

III. It is not located at its fiscal domicile or at the domiciles registered in the Program to carry out the operations under it, or said domiciles are in the event of not being located or non-existent;

…

1. Submit false documentation, altered or with false data, or when the SAT determines that the name or fiscal address of the supplier or producer, recipient or buyer abroad, indicated in the petitions, invoices or the information transmitted in terms of the Law, are false, non-existent or not located;

The PROSEC Decree, indicates as cause for cancellation of the Program when the producer changes his fiscal domicile without presenting the corresponding notice to the Ministry of Finance and Public Credit.

ARTICLE 9.- The Ministry by itself or at the request of the Ministry of Finance and Public Credit will cancel the authorization of the respective program, without prejudice to applying other sanctions, when the producer is located in any of the following cases

III. Do not file three or more declarations of provisional payments or the declaration of the fiscal year of Income Tax, Asset Tax and Value Added Tax, or change your fiscal domicile without presenting the corresponding notice to the Ministry of Finance and Public Credit , or is not up to date with its tax obligations, or...

And in the Registry in the Business Certification Scheme in the VAT and IEPS and Certified Business Partner modalities, they are grounds for cancellation and suspension when the taxpayer is not located at their fiscal domicile or that of their establishments are in the event of not located or non-existent.

Causes for cancellation and suspension of the Registry in the Business Certification Scheme in the VAT and IEPS modalities and Certified Business Partner

7.2.4. The AGACE will proceed to start the cancellation procedure of the Registration in the Company Certification Scheme granted in terms of rules 7.1.2., 7.1.3. and 7.1.5., for any of the following reasons:

General causes:

…

VII. The taxpayer is not located at his fiscal domicile or that of his establishments are in the event of not located or non-existent.

As can be seen from the aforementioned legal provisions, the fiscal domicile acquires relevance in the foreign trade operation, since, if the authority determines that it is NOT LOCATED, NON-EXISTENT or is not UPDATED, it can have as a consequence , the suspension or cancellation of the registers, programs or registries in which it is registered, with the corresponding sanction, as the case may be, as well as the affectation in your customs operation.

WHAT SHOULD I TAKE CARE OF?

THE QUALIFICATION OF THE AUTHORITY

The AGACE, the AGAFF, the AGSC and now the ANAM, within the sphere of their powers, can QUALIFY the FISCAL ADDRESS of taxpayers in three areas:

- Located Address - Taxpayer not located

- Address Not Located

- Does not meet any of the requirements of article 10 of the CFF: More than one taxpayer at home. Remarkably small surface dimensions.

Considering the above, to avoid falling into a bad rating by the authority, the following suggestions are made:

a) If you are a company that has been carrying out foreign trade operations for some time:

- Verify in your proof of tax situation that the status of the tax domicile is "LOCATED".

- Have at hand proof of address whose data coincides with that indicated as TAX ADDRESS.

- Verify that the details of the street and number are visible on the façade of your location and coincide with the one indicated as FISCAL ADDRESS.

- In case of exercise of powers of verification by the authority, NEVER SAY that "it is not here", since the authority could determine the non-existence of the address.

- In the event that there is a change of address (for example, that the street name is changed, or there is a renumbering), it will be necessary to carry out the update process before the RFC, as well as request the VERIFICATION OF ADDRESS.

b) If you are a new company and you wish to enroll in the foreign trade registers, programs or registries, carry out these suggestions:

- Do your paperwork with the RFC and register the FISCAL ADDRESS.

- Request your ADDRESS VERIFICATION from the SAT.

- Your proof of address must coincide with the one indicated as TAX ADDRESS.

- Verify that the address that you indicate in the contracts that you will present to the authority coincides with the FISCAL ADDRESS.

- During the development of the RESIDENCY VERIFICATION, present the information requested by the authority.

Remember that currently the authority is very aware that the regulations on foreign trade are complied with, with semicolons, so they are looking for any fault, to give a bad rating to tax domiciles

En MDI TRADE SOLUTIONS, podemos ayudarte en caso de que estes en un supuesto de cancelación o suspensión de tus padrones, programas o registros si la causal está relacionada con el DOMICILIO FISCAL, y recuerda seguir la segunda parte, donde te diremos como se lleva a cabo una solicitud de VERIFICACIÓN DE DOMICILIO.